What to Check Before Buying a Prop Firm Challenge

What to Check Before Buying a Prop Firm Challenge: A 13-Point Due-Diligence Checklist

Here's what to check before buying a prop firm challenge: not the homepage, not the Instagram ad — the actual rulebook you'll be graded on. Most traders compare firms on price and profit split and stop there. That's backwards. Price is refundable in spirit (you can just not buy again); a vague rulebook costs you a passed evaluation you can never get back.

Why This Checklist Comes Before the Price Comparison

A challenge fee buys you an attempt, not a guarantee. What decides whether that attempt turns into a funded account is whether you knew the exact rules going in — not the marketing summary, the numbers.

Firms that are confident in their model publish those numbers before you pay. Firms that aren't tend to bury them in a Discord channel or a dashboard you only see after checkout. This is basically a prop firm due diligence checklist — the kind of due diligence you'd apply before any purchase this size — built to show you how to vet a prop firm in five minutes, before your card gets charged.

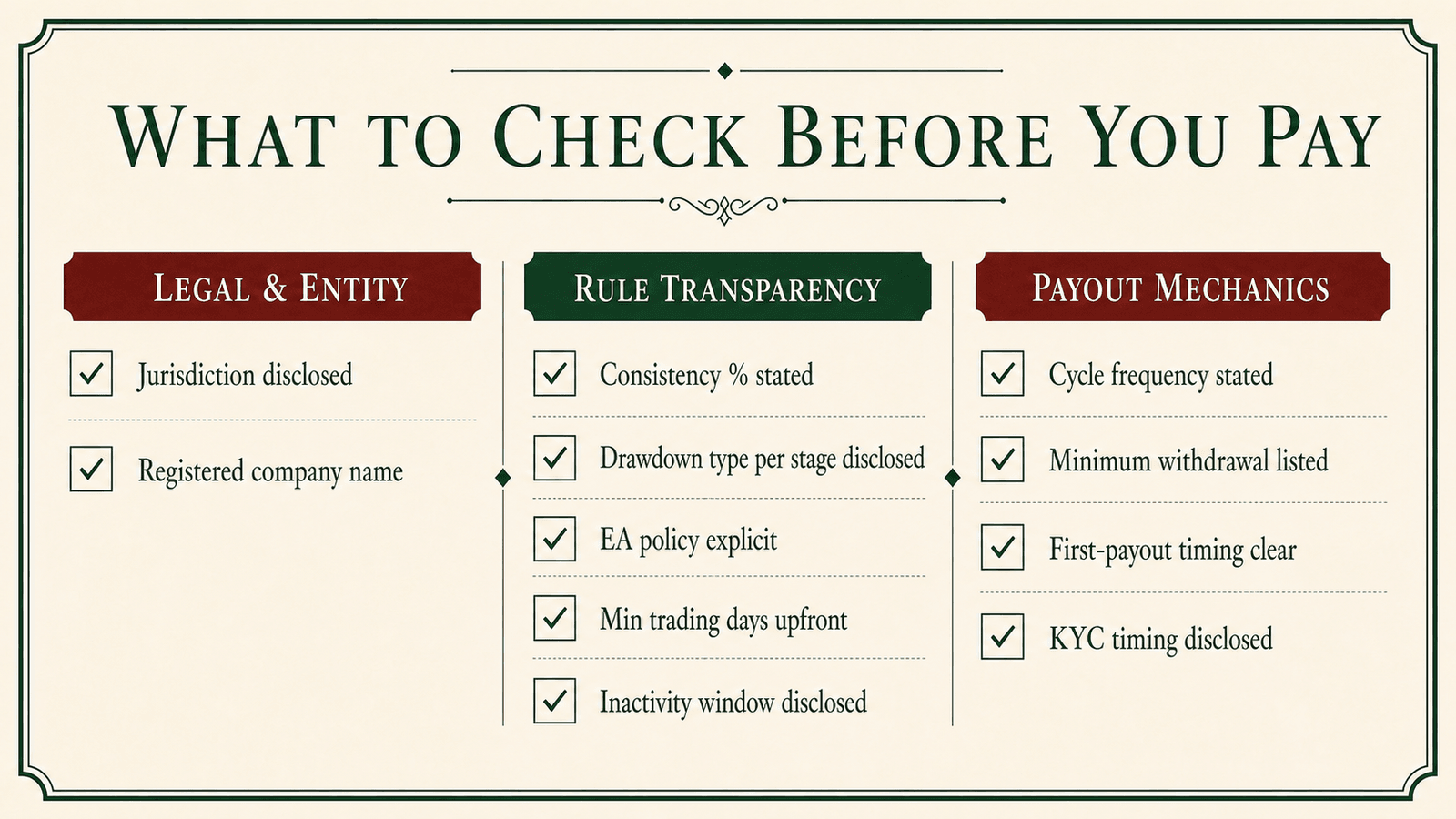

What to Check Before Buying a Prop Firm Challenge: The Full List

| # | What to check | Why it matters |

|---|---|---|

| 1 | Legal entity and jurisdiction, named | Tells you who you're actually contracting with, and where a dispute would even be heard. |

| 2 | Full rules linked at checkout, not summarized | A pricing-page summary isn't a contract; the rule sheet you agree to is. |

| 3 | Consistency rule stated as an exact percentage | "Trade consistently" is not a rule. "35%" is. |

| 4 | Drawdown type disclosed separately for evaluation vs. funded | Static and trailing drawdown behave very differently — see below. |

| 5 | News-event handling defined precisely | You need a blackout window in minutes, not "trade responsibly around news." |

| 6 | Numeric max lot size and leverage | "Reasonable risk" isn't enforceable; a lot cap and a leverage ratio are. |

| 7 | EA / bot policy spelled out | Determines instantly whether your strategy is even allowed. |

| 8 | Minimum trading days stated up front | Passing too fast, before this is met, can flag or delay you. |

| 9 | Inactivity window disclosed | Tells you how long you can go quiet before the account is at risk. |

| 10 | Payout mechanics: cycle, minimum, first-payout timing | The difference between "weekly" and "monthly, maybe" is real cash flow. |

| 11 | KYC requirements listed before purchase | You want to know your ID will clear before you've already paid. |

| 12 | Payment method and country restrictions | Some firms quietly block certain countries or payment rails after checkout. |

| 13 | Similarly-named-entity check | Prop firm names get cloned by lookalike sites; confirm you're on the real domain. |

Who exactly are you paying?

Start here, before you even open the pricing page. A legitimate firm names its legal entity and jurisdiction — not "a global company," an actual registered name you can look up. TBM Funded, for example, discloses that it's operated by TBM Capital L.L.C-FZ, registered in Meydan Free Zone, Dubai, UAE — that's item 1, checked, on our own How It Works page.

Item 13 sits right next to it for a reason: once a prop firm brand gets traction, lookalike domains and cloned social pages start showing up, especially around payout season when a firm's name is trending. Before you enter payment details anywhere, confirm the URL matches the firm's own links, not a result from a sponsored ad or a DM. Pair that with item 12 — check the accepted payment method and whether your country is quietly excluded — before you're mid-checkout and find out the hard way.

Are these the rules you'll actually be tested on?

This is where most due diligence stops too early. A firm can publish "up to 90% profit split" in bold on the homepage and still bury the consistency rule that determines whether you ever see that split. Ask for the exact percentage — not "consistent trading encouraged."

Drawdown is the other place vague language hides real risk. A firm should tell you, separately, whether your evaluation drawdown is static (fixed from your starting balance) and whether your funded account switches to trailing end-of-day (measured against your peak balance, which tightens the room you have as the account grows). These are genuinely different products with different risk, and a firm that doesn't separate them in writing hasn't actually told you the rule — see our full breakdown on static vs. trailing drawdown if the distinction is new to you.

The rest of items 5 through 9 are just specificity checks. "No trading during high-impact news" is not a rule; "no open or close within 5 minutes of a red-folder release" is. "Reasonable lot sizes" is not a rule; "20 lots max, 1:100 leverage" is. If you run an EA, get the bot policy in writing before you buy — most firms allow a personally-owned EA with proof of ownership on request, and ban third-party or commercial EAs outright. Minimum trading days matters more than it sounds: passing a phase too fast, before the minimum is met, is one of the most common reasons an otherwise-clean pass gets held for review.

What happens after you pass?

This is where firms lose traders who did everything right. Check the payout cycle length, the minimum withdrawal amount, and how many days after activation the first payout becomes eligible — all three, together, before you pay. "Payouts available" tells you nothing; "weekly, $50 minimum, first payout after 14 days plus 3 trading days" is something you can plan around.

KYC deserves the same scrutiny. A trustworthy firm lists its verification requirements before purchase, not the day you request a withdrawal — that way a document mismatch surfaces early, not as a payout delay with your money already committed. And check the inactivity window: how long can the account sit untouched before it's closed, and what happens to any pending balance if it is.

How TBM Discloses This (One Example, Not a Pitch)

You don't need to take our word that this checklist is usable — here's how it maps to TBM's own published rules, so you can see what a filled-in version looks like.

| Checklist item | 2-Phase | Rapid |

|---|---|---|

| Targets (P1 / P2) | 8% / 5% | 6% / 6% |

| Max drawdown (evaluation) | 10% (static) | 6% (trailing) |

| Daily drawdown | 5% | 3% |

| Min trading days per phase | 5 | 3 |

| Time limit | No time limit | No time limit |

| Leverage | 1:100 | 1:100 |

| Profit split | 80% | 90% |

Funded-stage rules are shared across both products: drawdown moves to trailing end-of-day (never static once funded), consistency is capped at 35% of total profit on a single day with a soft-hold on breach (not termination), payouts run weekly in USDT with a $50 trader minimum, and the first payout is eligible after 14 days plus 3 trading days. KYC is required at funded-account issuance, not withdrawal. Capital is simulated — you never deposit money to trade the account, you pay a one-time evaluation fee and real USDT flows out on payout. Global marketing on TBM properties says "up to 90%" split, because the exact number depends on which product you buy; see Pricing for the product-specific breakdown before you choose.

None of this means TBM is the only firm doing it right, or that you should buy from us specifically. It means these 13 answers should exist, in writing, for any firm you're evaluating — and if a firm can't produce them before you pay, that's not a minor gap. Treat a firm's payout rules that are vague on cycle, minimum, or first-payout timing as a genuine prop firm red flag, not a detail to sort out later.

FAQ

What's the single most important thing to check before buying a prop firm challenge? Whether the full rule set — not a homepage summary — is linked and readable before you pay. Everything else on this list (drawdown type, consistency percentage, payout timing) should live inside that document, not scattered across a dashboard you only see after checkout.

How do I know if a prop firm is legit before paying? Check for a named legal entity and jurisdiction, a real domain that matches the firm's own marketing links, and published KYC requirements. A firm that's vague about who it legally is, or that only asks for verification after you've paid, is a red flag regardless of how good its pricing looks.

What's the difference between static and trailing drawdown, and why does it matter here? Static drawdown is fixed against your starting balance and common during evaluation. Trailing drawdown recalculates against your account's peak balance and is common once you're funded — it's tighter by design. A trustworthy firm states which applies at which stage; see our full explainer.

Why does the consistency rule matter so much before I buy? It caps how much of your total profit can come from one outsized day, usually as a percentage. If a firm won't give you that exact number, you can't plan your trading around it — and a breach later can hold up a payout you thought was already earned. Full detail in our consistency rule explainer.

Should I still check anything after I've already passed the evaluation and gotten funded? Yes. Passing doesn't retire the rulebook — drawdown limits, the inactivity window, and KYC can all still affect a live payout. For the specific ways a funded account can lose a payout after passing, see our payout denials checklist.

More questions like these are answered in our full FAQ.

Risk disclaimer: Trading forex and CFDs carries real risk and can result in loss of your capital. Prop firm challenges involve fees and don't guarantee funding or income. This isn't financial, legal, or tax advice — see our full Risk Disclosure.

Last updated: July 15, 2026