Static vs Trailing Drawdown: The Rule Traders Get Wrong

Static vs Trailing Drawdown: The Rule Traders Get Wrong

Static vs trailing drawdown: two rules that share a name and nothing else.

Here's an uncomfortable truth: most traders don't fail a prop firm challenge because they can't trade. They fail because they never actually understood their drawdown rule. And there are two totally different versions of it hiding under the same name.

Let's fix that in five minutes.

Static vs trailing drawdown: what the words actually mean

Your max drawdown is the ceiling — how much your account can drop from its high point before you're out (a peak-to-trough decline, in finance terms). Simple enough. The part that trips people up isn't the number. It's how the ceiling moves.

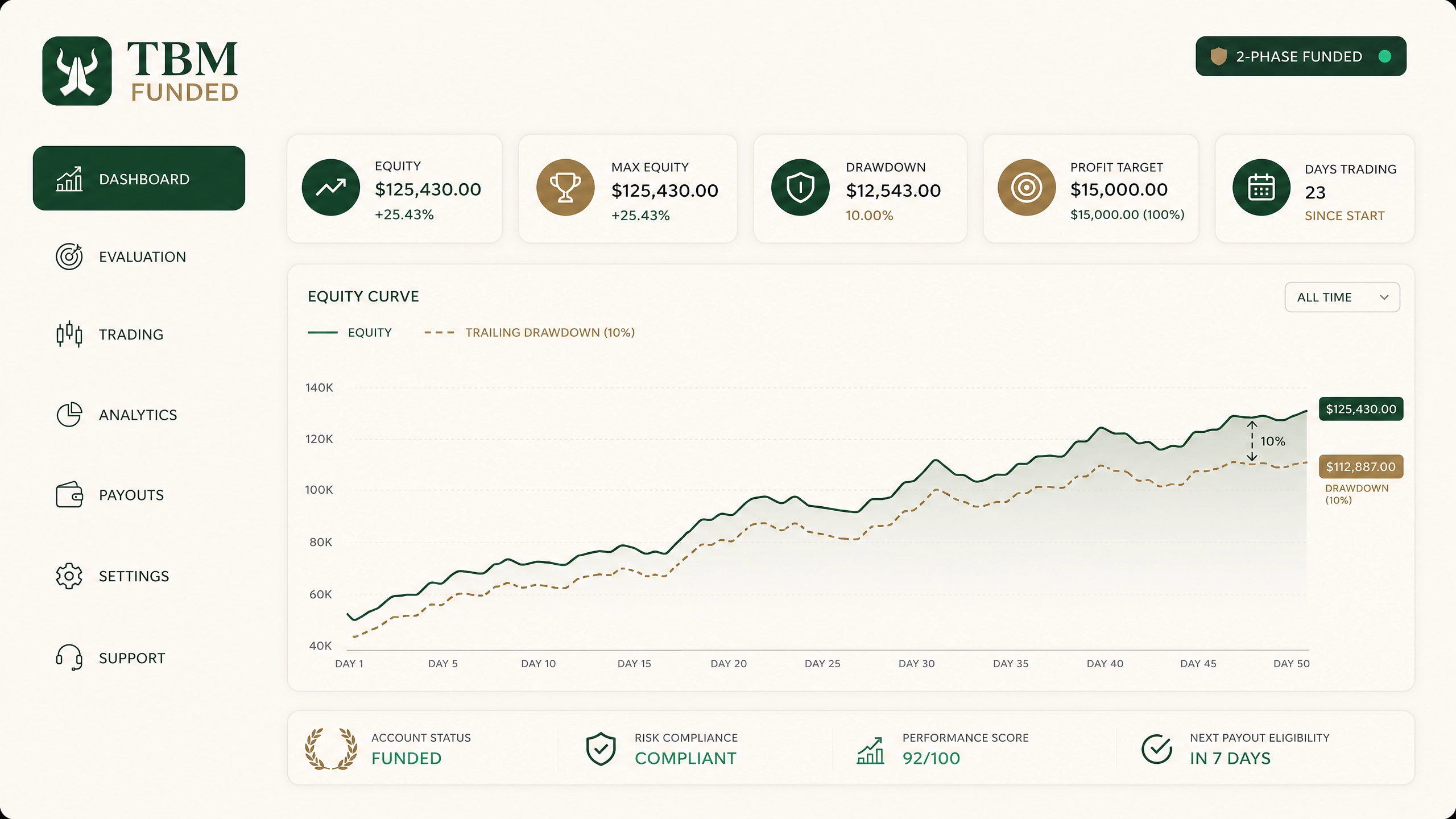

Static drawdown — the ceiling stays put

With static drawdown, your limit is locked to your starting balance. Say you start with $25,000 and your max drawdown is 10%. Your floor is $22,500. Full stop. It doesn't matter if you grow the account to $30,000 first — your floor stays at $22,500 the whole time.

This is the friendlier version. Once you've built a cushion, that cushion is genuinely yours.

Trailing drawdown — the ceiling follows you

Trailing drawdown moves with your highest ever balance, not your starting one. Grow that same $25,000 account to $30,000, and your floor doesn't stay at $22,500 — it jumps to $27,000 (10% below your new high). You just made $5,000, and your safety margin shrank instead of growing.

This is the version that quietly ends accounts. Traders assume profit means more breathing room. With trailing drawdown, profit can mean less.

Why this actually matters more than your profit split

You can have the best split in the industry and still blow an account because you didn't know which version you were trading under. This single rule decides more outcomes than almost anything else in your contract. Read it before you read anything else.

Where TBM Funded stands

Here's exactly how we run it, product by product — full rules live on How It Works — no fine print games:

On our 2-Phase evaluation: static drawdown, 10% max / 5% daily, locked to your starting balance from day one. Once you're funded, it trails end-of-day — same 10% max / 5% daily, just now measured against your highest balance instead of your starting one.

On Rapid: trailing drawdown from day one of the evaluation — 6% max / 3% daily, tighter than 2-Phase because Rapid gets you funded faster and pays a higher 90% split. Your floor rises with your balance from the moment you open the evaluation, not just once you're funded — the same 6% max / 3% daily mechanic carries straight through, with no change at the funding milestone. We don't loosen the rule just because you're funded — the number that got you there is the number you trade under, and for Rapid, the type was never static to begin with.

| Product | Evaluation drawdown | Funded drawdown | Profit split |

|---|---|---|---|

| 2-Phase | Static 10% max / 5% daily | Trailing 10% max / 5% daily | 80% |

| Rapid | Trailing 6% max / 3% daily | Trailing 6% max / 3% daily | 90% |

(Current numbers always live on Pricing.)

Two products, two different limits, and now you know both — before you pay, not after.

How to actually protect yourself

Ask any firm you're considering one direct question: "Is my drawdown calculated from my starting balance, or my highest balance ever reached — and does that change once I'm funded?" If they can't answer that in one sentence, that's your answer too.

Quick questions

Is trailing drawdown always worse? Not worse — different. It's common on funded accounts industry-wide. The problem isn't the rule. It's traders not knowing which one applies at which stage.

Does TBM Funded use trailing drawdown during the evaluation? On 2-Phase, no — evaluation is static, locked to your starting balance, and trailing only applies once you're funded. On Rapid, yes — evaluation drawdown is trailing from day one, the same mechanic Rapid uses once funded. The two products are no longer identical on this point.

Does the drawdown limit change once I'm funded? On 2-Phase, yes — the type changes from static to trailing (the percentage stays the same, 10% max / 5% daily). On Rapid, no — drawdown is trailing throughout, both evaluation and funded, so nothing about the mechanic changes at the funding milestone. Either way, the percentage you evaluated under is the percentage you trade funded — 2-Phase's 10%/5% or Rapid's tighter 6%/3%.

How do I calculate my actual floor? Take your account size, multiply by your product's max drawdown percentage, subtract from either your starting balance (static, evaluation) or your highest-ever balance (trailing, funded).

More rule questions like these are answered in our full FAQ.

Risk disclaimer: Trading forex and CFDs carries real risk and can result in loss of your capital. Prop firm challenges involve fees and don't guarantee funding or income. This isn't financial, legal, or tax advice — see our full Risk Disclosure.