2-Phase vs Rapid: Which TBM Challenge Fits You?

2-Phase vs Rapid: Which TBM Challenge Fits Your Trading Style?

2-Phase vs Rapid: which TBM challenge fits your trading style depends less on "which one is better" and more on what you're actually optimizing for — room to breathe, or a bigger split and fewer days to clear.

Both are real, live products you can buy today. Both get you to a funded account with real USDT payouts, up to 90% split across the lineup. The difference is in the rulebook, and the rulebook decides which one suits how you actually trade.

2-Phase vs Rapid: which TBM challenge fits your trading style — the numbers

Here's the full rule set for both, side by side.

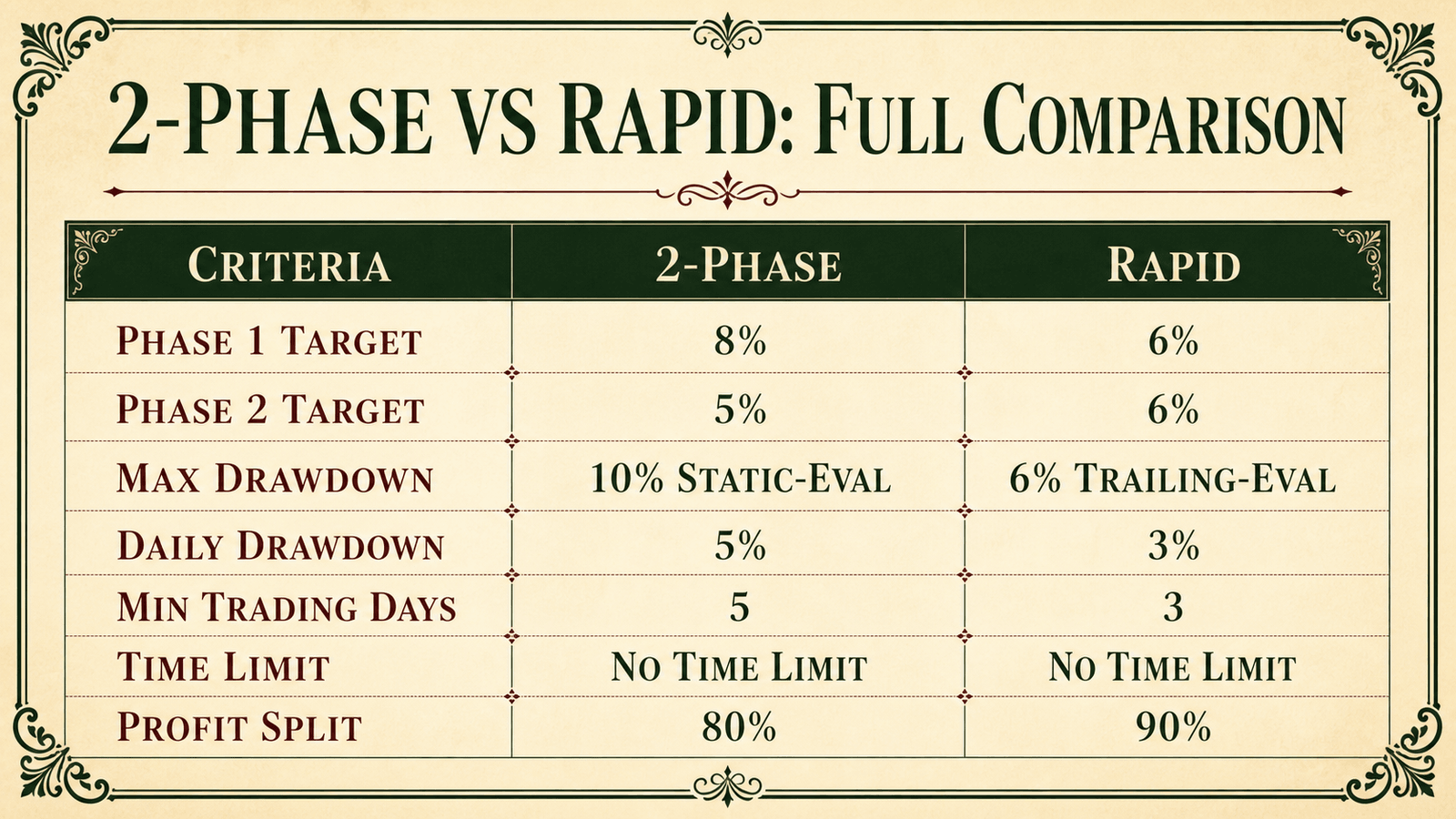

| Rule | 2-Phase | Rapid |

|---|---|---|

| Phase 1 target | 8% | 6% |

| Phase 2 target | 5% | 6% |

| Max drawdown (evaluation) | 10%, static | 6%, trailing |

| Daily drawdown | 5% | 3% |

| Minimum trading days per phase | 5 | 3 |

| Time limit per phase | No time limit | No time limit |

| Leverage | 1:100 | 1:100 |

| Profit split once funded | 80% | 90% |

Everything else — instruments traded, max loss per trade, position size, inactivity rule, payout mechanics — is identical across both, including leverage at 1:100. Read on for what each number actually means for your day-to-day trading.

What 2-Phase gives you

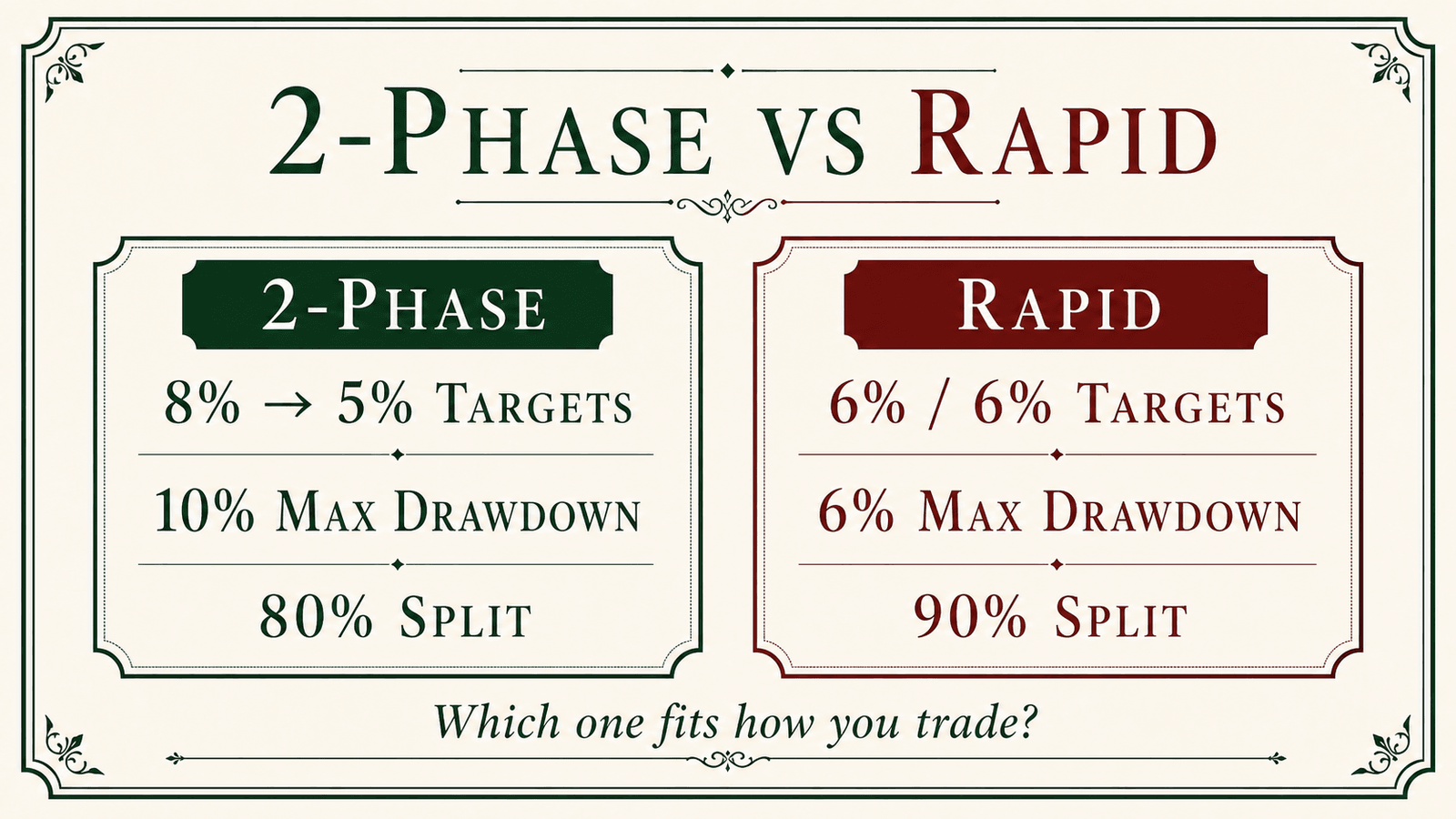

2-Phase is the flagship for a reason: it's built for room. Phase 1 asks for an 8% gain, Phase 2 for 5%, and your 10% max drawdown is locked to your starting balance the whole way through — static, not trailing, during the evaluation.

Daily drawdown sits at 5%. That's forgiving enough to absorb a rough session without ending your attempt on the spot. You also get 5 minimum trading days per phase to work with, and there's no time limit on the phase itself — plenty of space if you trade a handful of times a week rather than every single day.

The tradeoff: once funded, you keep 80% of what you earn. Solid, but the lowest split TBM offers.

What Rapid gives you

Rapid earns its name. Phase 1 and Phase 2 both ask for a flat 6%, your max drawdown is tighter at 6%, and daily drawdown drops to 3%. You only need 3 minimum trading days per phase — the lowest bar on the board.

Tighter numbers mean less margin for error. A 3% daily drawdown punishes a bad morning harder than 2-Phase's 5% does, and a 6% max drawdown gives you less total room before you're out. In exchange, once you're funded, you keep 90% of your profit — the top split TBM offers on any product.

Rapid rewards traders who already run tight risk management: small, controlled losses per trade, no revenge trading, no letting one day swing the whole account.

Drawdown: static vs trailing, and when each applies

This part trips people up, so get it straight before you buy either one. Drawdown is the peak-to-trough decline your account is allowed before you're out. During the evaluation phase, 2-Phase uses static drawdown — your floor is locked to your starting balance and doesn't move even as you grow the account. Rapid's evaluation runs on trailing end-of-day drawdown already — your floor follows your highest balance reached, checked once per day at market close, from day one of the challenge.

Once you're funded, both products run on trailing end-of-day drawdown — 10% max / 5% daily for 2-Phase, 6% max / 3% daily for Rapid. Same percentages you evaluated under, different reference point. For 2-Phase, that's a real shift from the static floor you traded under during evaluation. For Rapid, nothing changes at the funding line — you're already on trailing drawdown from the first day of Phase 1 straight through to a funded account. Our static vs trailing drawdown breakdown covers the mechanics in full if you want the deeper explanation.

Profit split: 80% vs 90%, and why both matter

TBM's global split claim is "up to 90%" because the two products genuinely sit at different points. 2-Phase pays a flat 80% once funded. Rapid pays 90% — the number the "up to" refers to.

A wider split sounds like the obvious pick, but it only pays off if you can actually operate inside Rapid's tighter drawdown rules. Someone who trades within 2-Phase's rules but breaches Rapid's 6% max drawdown every third attempt isn't actually better off chasing the bigger number. This is really a question of risk tolerance — how much room you genuinely need versus how much you're willing to give up to trade with less of it.

Who should pick 2-Phase

- You hold trades for hours or days, not seconds, and want your stop-loss room to match.

- You don't trade every day and want no time limit on the phase, just 5 minimum trading days to clear.

- You're newer to funded evaluations and want the friendlier 10% max / 5% daily buffer while you learn how a live drawdown rule actually feels.

- You'd rather bank a solid 80% split than risk more breaches chasing 90%.

Who should pick Rapid

- Your risk management is already tight — small stops, consistent position sizing, no oversized days.

- You want to clear the minimum-trading-days requirement fast: 3 days per phase instead of 5.

- The bigger 90% split matters more to you than extra drawdown room, and you're confident you won't need it.

- You trade with discipline on quiet days as much as active ones — a 3% daily drawdown doesn't leave space for one loose session to undo the rest of the week.

Fees by account size

Both products run the same five account sizes — Soldier through Don — at different one-time evaluation fees.

| Tier | Size | 2-Phase fee | Rapid fee |

|---|---|---|---|

| Soldier | $5,000 | $36 | $45 |

| Capo | $10,000 | $66 | $79 |

| Mad Men | $25,000 | $156 | $189 |

| Boss | $50,000 | $289 | $349 |

| Don | $100,000 | $529 | $629 |

Rapid costs more upfront across every tier — you're paying for the bigger split and the shorter minimum-trading-days bar, not for easier targets. Current pricing is always live on Pricing; the numbers above are ground truth as of this post.

Payouts work the same either way

Once funded on either product, your first payout is available after 14 days on the account plus a minimum of 3 trading days. Your first two payouts are capped at 6% of account balance each; after that, the cap lifts and payouts run weekly, in USDT, with a $50 minimum withdrawal.

The consistency rule applies to both products the same way too: no single trading day can be more than 35% of your total profit at payout time. A breach puts that payout cycle on a soft hold for review — it doesn't end your account. Full walkthrough of the process, including what each phase actually checks, is in How It Works.

The honest capital framing

Whichever you pick, remember what a funded account actually is: simulated capital, real USDT payouts. You never deposit your own money to trade the account — the one-time evaluation fee above is the only money you put in. Everything you earn from that point is paid to you, at your split, in real USDT.

Quick questions

Which is easier to pass, 2-Phase or Rapid? Neither is "easier" — they trade off different things. 2-Phase gives you more room (10% max drawdown, 5% daily, static evaluation drawdown) but pays 80%. Rapid is tighter (6% max drawdown, 3% daily, trailing evaluation drawdown) but pays 90% and needs fewer minimum trading days. Neither has a time limit on the phase.

Can I switch from one to the other later? Yes. Nothing locks you into one product — buy whichever evaluation fits how you trade right now, and run the other one next time if it suits a different setup.

Does the drawdown work the same way on both once I'm funded? Both run on trailing end-of-day drawdown once funded, checked once per day at close against your highest balance reached — 10%/5% daily for 2-Phase, 6%/3% daily for Rapid. During the evaluation itself, 2-Phase stays static while Rapid is already trailing, so funding doesn't change anything for Rapid's drawdown mechanic.

Is Rapid actually riskier because the drawdown is tighter? It demands tighter per-trade discipline, not more risk-taking. A 6% max drawdown with the same 2% max-loss-per-trade rule still gives you real working room — it just leaves less margin for a bad stretch than 2-Phase's 10%.

Which one gets me to a payout faster? Rapid's 3 minimum trading days per phase (versus 5 for 2-Phase) means you can clear the trading-day requirement sooner if you're active daily. Actual funding speed still comes down to hitting your profit targets, not just clocking days — see the full rulebook in our 2-Phase challenge rules breakdown and compare it against what you just read here for Rapid.

Risk disclaimer: Trading forex and CFDs carries real risk and can result in loss of your capital. Prop firm challenges involve fees and don't guarantee funding or income. This isn't financial, legal, or tax advice — see our full Risk Disclosure.