Why Prop Firm Payments Keep Getting Declined

Why Your Prop Firm Payments Keep Getting Declined

Prop firm challenge payments get declined far more often than typical online purchases because card networks classify trading-evaluation merchants as high-risk, cross-border card-not-present transactions trigger extra fraud scoring, and issuing banks apply stricter holds on unfamiliar merchant category codes. A decline usually signals a processor or bank-side flag — not proof the firm itself is untrustworthy.

If you've tried to pay for a challenge and watched your card get rejected two or three times in a row, you're not imagining a pattern. It's a mechanical one, and it has almost nothing to do with your bank balance.

The Real Reason Card Payments Fail (Not What Most People Think)

Most traders assume a decline means "insufficient funds" or "my bank blocked international spending." Sometimes that's true. But the more common cause sits upstream, in how card networks classify the merchant on the other end.

Businesses that sell trading evaluations, simulated funding, or anything adjacent to financial speculation often get grouped under merchant category codes (MCCs) that card networks and acquiring banks treat as elevated-risk — the same bucket used for online trading platforms, forex education, and other financial-services products sold purely online. That classification matters because both Visa and Mastercard run formal dispute-monitoring programs (Visa's Dispute Monitoring Program and Mastercard's Excessive Chargeback Program are the two most cited) that track a merchant's chargeback-to-transaction ratio. Merchants who sit in a risk-sensitive category get watched more closely under these programs, and acquiring banks respond by tightening authorization rules for that entire category — sometimes before a single dispute has even happened on a specific account.

The result: your card can be declined not because you did anything wrong, and not because the firm has a bad track record, but because the underlying merchant classification puts extra friction on every transaction that passes through it.

Chargeback Risk Isn't Unique to Any One Firm

This is a structural feature of how card networks price risk for an entire category of digital-first, subscription-adjacent, financial-education businesses — not a signal about any specific company's reliability. A firm with a clean track record and a firm with real problems can both trigger the exact same category-level friction, because the flag is attached to the type of transaction, not the merchant's history.

Card-Not-Present + Cross-Border = A Double Risk Flag

Two separate risk signals stack on top of each other in a typical prop firm purchase, and together they explain most of the declines that have nothing to do with the merchant at all.

Card-not-present (CNP) risk. Any transaction where the physical card isn't swiped or tapped carries inherently higher fraud scoring than an in-person purchase, because the issuing bank can't verify the chip or PIN. E-commerce in general absorbs this cost; prop firm checkouts absorb it on top of a risk-sensitive MCC.

Cross-border risk. When the cardholder's issuing country doesn't match the merchant's registered processing country, fraud models built into the issuing bank's authorization system treat the mismatch as a meaningful risk input — sometimes enough on its own to trigger an automatic decline or a manual review hold. Add a currency conversion, an AVS (address verification) mismatch because billing details don't map cleanly to the merchant's system, or a failed 3D Secure / Strong Customer Authentication step, and the transaction has multiple independent reasons to fail before it ever reaches a human.

None of this requires anything to be wrong with the trader's card or the firm's payment page. It's the combination of CNP plus cross-border plus category risk that compounds.

Why the Friction Hits Some Traders Harder Than Others

The compounding effect above isn't evenly distributed. Wherever outbound cross-border card spend already carries added intermediary bank fees, tighter currency-conversion controls, or issuing banks tuned to flag unfamiliar foreign merchants more aggressively, the baseline decline rate for exactly this kind of purchase runs structurally higher — independent of the trader's credit history or the merchant's legitimacy. If your card routinely gets extra scrutiny on any cross-border, foreign-currency, card-not-present purchase — not just prop firm challenges — that's the same underlying mechanism, not a coincidence specific to this industry.

This is also why demand for non-card settlement — stablecoins in particular — has grown fastest precisely in the markets where card-rail friction is worst. It's not a preference; it's traders routing around a bottleneck.

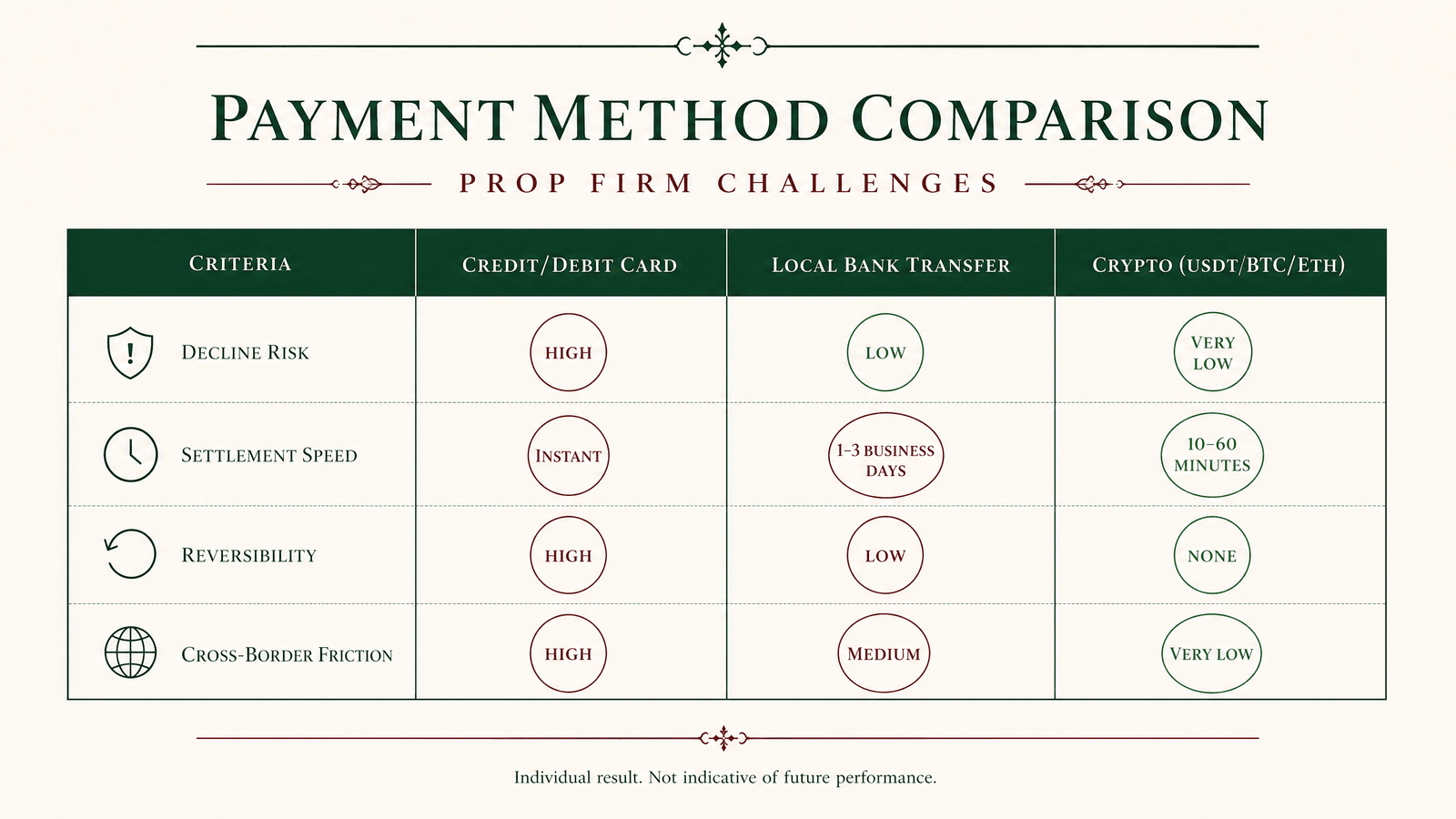

Payment Method Comparison: What Actually Clears

| Method | Typical decline risk | Settlement speed | Reversibility | Cross-border friction |

|---|---|---|---|---|

| Credit/debit card (CNP, cross-border) | High — stacked risk flags | Instant if approved | Reversible (chargeback) | High (FX, AVS, 3DS) |

| Local bank transfer / instant payment rail | Low-moderate | Minutes to 1 business day | Usually irreversible once cleared | Low if same-currency |

| Crypto (BTC, ETH, USDT) | Very low — no card network involved | Minutes (network-dependent) | Irreversible | None — no FX conversion, no issuing bank in the loop |

Crypto isn't "safer" in a security sense — it's structurally different. There's no card network, no issuing bank fraud model, and no MCC classification sitting between the trader and the payment. That's precisely why it clears where cards don't: the entire decline mechanism described above simply doesn't apply.

What Actually Works

Stablecoins and major crypto (USDT, BTC, ETH). Settlement doesn't pass through a card network or a correspondent bank chain, so there's no cross-border authorization step to fail. Confirmation is typically visible on-chain within minutes, and the trader controls the transaction end to end. This is why TBM Funded's own checkout runs on USDT rather than cards — see How It Works for the full payment flow.

Region-specific instant payment rails. Where available, domestic real-time transfer networks avoid the cross-border flag entirely because both sides of the transaction sit inside the same banking system — no currency conversion, no foreign-merchant classification.

Retrying with a different card or issuer. Not all banks apply the same fraud-scoring thresholds. A decline on one card doesn't predict a decline on another, since each issuer sets its own tolerance for cross-border CNP risk.

How to Tell a Processor Decline From an Actual Red Flag

A decline is a normal, expected part of cross-border card payments — it's not evidence of anything by itself. Before concluding a firm is untrustworthy, check:

- Does the firm name a real, identifiable payment processor (a known crypto payment gateway, a recognized card processor) rather than routing payment to a personal wallet or personal bank account with no invoice trail?

- Do you receive an order ID, transaction reference, or confirmation email regardless of whether the payment succeeded or failed? Legitimate processors generate these automatically.

- Is the requested payment method unusual — gift cards, untraceable wallet transfers with no memo, or "send to this personal handle" instructions? That combination is a genuine warning sign, distinct from a standard card decline.

- Can you verify the firm's terms, refund policy, and rules independently, before payment, rather than only after you've already paid?

A card decline tells you about your card issuer's risk model. It tells you nothing about the firm's legitimacy on its own — that requires checking the firm's own published terms and payment infrastructure separately. For a look at what those published terms should cover, see our prop firm payout denials checklist.

FAQ

Why does my card keep getting declined when I try to pay for a prop firm challenge? Most declines on prop firm purchases come from a combination of card-not-present risk, cross-border authorization flags, and the merchant category classification carried by trading-evaluation businesses — not from your account balance or credit standing. Issuing banks apply extra fraud scoring to this combination before the transaction ever reaches the merchant.

Is it safe to pay for a prop firm evaluation with crypto? Crypto payments (BTC, ETH, USDT) avoid the card-network and cross-border authorization chain entirely, which is why they clear more reliably. Safety still depends on using a verified payment gateway and confirming the transaction address and amount before sending — those steps matter regardless of payment method.

Does a payment decline mean a prop firm is a scam? No. A decline reflects your card issuer's risk model responding to cross-border, card-not-present, high-risk-category signals. It's a separate question from whether a firm's terms, rules, and payout process are legitimate — verify those independently through the firm's published policies.

Why do cross-border card payments get flagged as high risk? Issuing banks weigh several signals together: the card isn't physically present, the billing country doesn't match the merchant's processing country, currency conversion is involved, and the merchant category itself may already carry elevated dispute-monitoring attention from the card networks. Any one of these can trigger a decline; together they compound.

What payment method has the lowest decline rate for prop firm challenges? Crypto settlement (BTC, ETH, USDT) and same-currency domestic instant payment rails both bypass the specific mechanisms — CNP scoring, cross-border authorization, MCC-based dispute monitoring — that cause most card declines in this category.

More questions like these are answered in our full FAQ.

Risk disclaimer: Trading forex and CFDs carries real risk and can result in loss of your capital. Prop firm challenges involve fees and don't guarantee funding or income. This isn't financial, legal, or tax advice — see our full Risk Disclosure.

Last updated: July 12, 2026.