Prop Firm Challenge $5,000 Account: Cost & Rules

Prop Firm Challenge $5,000 Account: What It Actually Costs at TBM Funded

Searching "prop firm challenge $5,000 account" usually means one thing: you want to start small and see if this whole funded-trading thing is even real, without betting a lot on it. Fair question. Here's the actual math — not the marketing version.

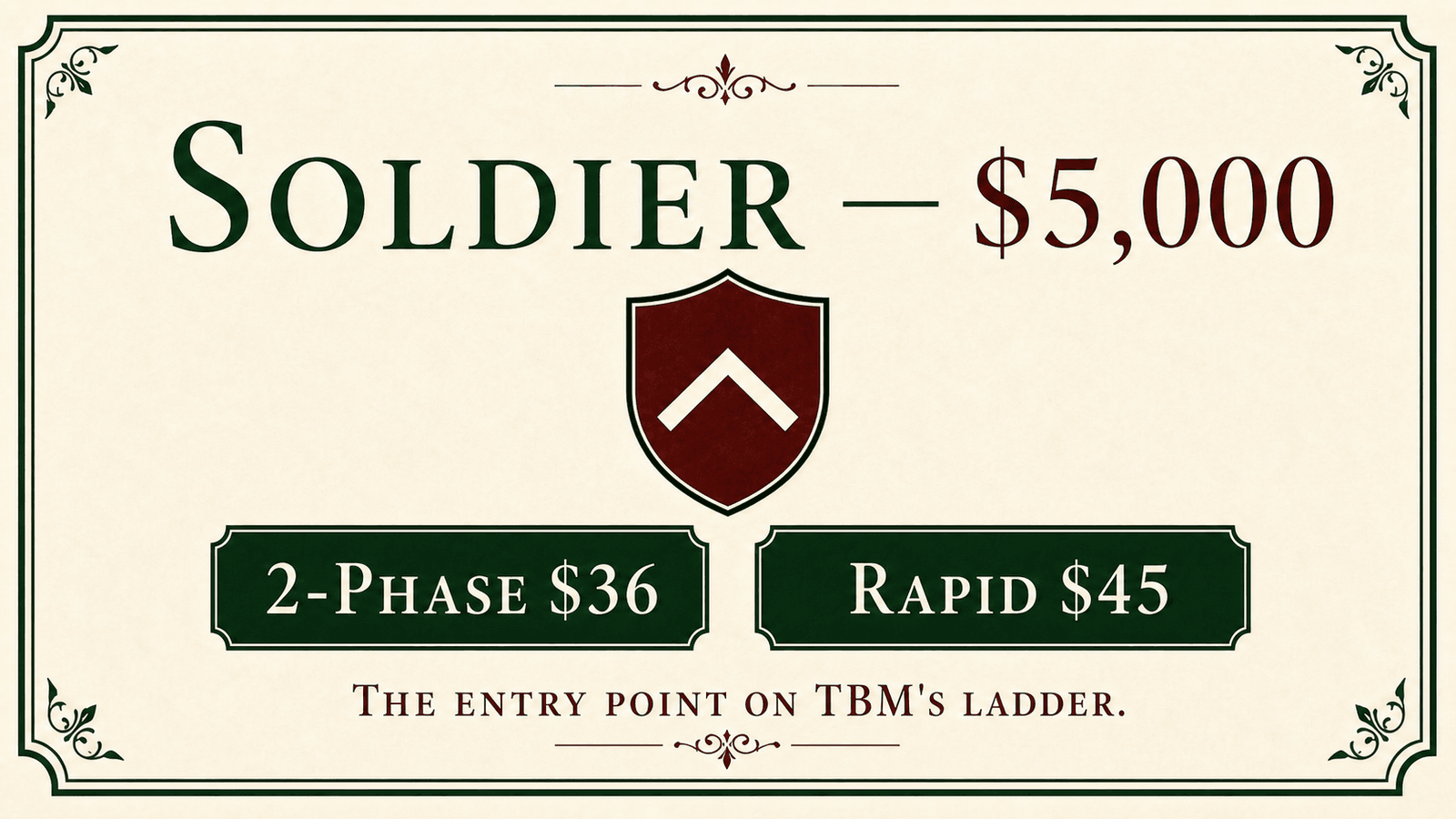

At TBM Funded, $5,000 is our smallest size — the Soldier tier, our entry-level prop firm challenge. It's built exactly for this: testing the model before you commit more, without the full prop firm challenge cost of a bigger size.

What does a prop firm challenge $5,000 account actually cost?

Two products, two prices, both one-time and paid in USDT — no subscription, no recurring charge.

| Product | Fee | Split once funded |

|---|---|---|

| 2-Phase (flagship) | $36 | 80% |

| 2-Phase Rapid | $45 | 90% |

That's it. You pay once to attempt the evaluation. You never deposit trading capital — the $5,000 balance is simulated, and it's TBM's number to risk, not yours. If you pass and get funded, the money you earn from it is real and paid out in USDT.

Soldier ($5K) rules at a glance

Here's every number that governs a $5,000 account, side by side, so you're not hunting through two separate pages.

| Rule | 2-Phase | Rapid |

|---|---|---|

| Phase 1 target | 8% | 6% |

| Phase 2 target | 5% | 6% |

| Max drawdown (evaluation) | 10% (static) | 6% (trailing) |

| Daily drawdown | 5% | 3% |

| Min trading days per phase | 5 | 3 |

| Time limit | No time limit | No time limit |

| Leverage | 1:100 | 1:100 |

| Profit split once funded | 80% | 90% |

2-Phase's max drawdown is static during the evaluation — locked to your $5,000 starting balance, so growing the account doesn't shrink your floor. Rapid's evaluation drawdown, by contrast, is trailing end-of-day — it tracks your highest balance reached from day one. Once either product is funded, drawdown switches to (or stays) trailing end-of-day against your highest balance reached, at the same percentage. Static and trailing are genuinely different rules that get mixed up constantly — we've broken down exactly how in static vs trailing drawdown if you want the full picture.

Who does a $5K challenge actually make sense for?

Three kinds of traders, honestly:

You're new to funded evaluations. A $36 or $45 fee is a cheap way to learn how the rules feel under real conditions — daily drawdown, consistency checks, the works — before you spend more on a bigger size.

You're testing a strategy, not your bank account. If you already trade well but want to see how your system holds up against someone else's rules, Soldier is the low-cost way to find out.

You want proof before you scale. Pass at $5K, and you can requalify at a bigger size later. Nobody's forcing you to jump straight to Don ($100K) on your first attempt.

If you already know you can pass consistently and $36-$45 isn't a meaningful amount to you, there's an argument for starting bigger — the rules are identical across every tier, only the account size and fee change. Full breakdown of every tier's rules lives on How It Works.

What can you realistically expect from your first payout?

This is the part most articles skip, and it matters more at $5K than at any other size.

Payouts run weekly, in USDT, with a $50 minimum withdrawal. Your first payout becomes available after 14 days on the funded account, plus a minimum of 3 trading days. So far, same for everyone.

Here's the part specific to smaller accounts: your first two payouts are capped at 6% of your balance each, regardless of your split. On a $5,000 account, 6% is $300. That cap applies whether you're on 2-Phase's 80% split or Rapid's 90% — it's a balance-based ceiling, not a split-based one, and it exists so early payouts don't drain a fresh account before it's had time to compound.

Run the numbers honestly: if you make $500 profit in your first payout window, your split (80% or 90%) would normally mean $400-$450. But the 6% cap on a $5,000 balance limits that first payout to $300, with the rest rolling forward. After your first two payouts, the cap lifts and you're paid your full split with no ceiling.

Bottom line — a small prop firm account like Soldier is a real way to get paid, but the first month's numbers on a $5,000 funded account will look modest by design. That's the honest trade-off for the lower entry fee.

2-Phase vs Rapid at $5K: which one fits you?

2-Phase gives you more room — 8%/5% targets, wider 10% drawdown, 5 trading days minimum per phase — in exchange for the lower 80% split. Rapid tightens everything (6%/6% targets, 6% trailing drawdown, only 3 minimum trading days) and pays 90% once you're funded, but the tighter drawdown means less margin for a bad week.

Neither is "better" — they're built for different trading styles. If you're still deciding, Pricing shows both side by side with live numbers for every account size, not just Soldier.

Quick questions

Do I need $5,000 of my own money to start? No. The $5,000 is simulated capital TBM provides once you pass the evaluation. You only ever pay the one-time evaluation fee — $36 for 2-Phase or $45 for Rapid.

Is $5,000 too small to make real money from? It's the smallest tier, so early payouts are naturally smaller — especially with the 6% cap on your first two payouts. Real money still moves in real USDT; it's just paced slower at this size than at Boss or Don.

Can I upgrade to a bigger account later? Yes. Passing a $5K evaluation doesn't lock you in — you can attempt a larger size whenever you're ready, at that tier's own fee.

Is the drawdown different at $5K than at bigger sizes? No. Drawdown percentages are identical across every account size for a given product — 10%/5% on 2-Phase, 6%/3% on Rapid. Only the dollar amount they represent changes with balance.

More questions like these are answered in our full FAQ.

For the complete 2-Phase rulebook — fees, EA policy, and every clause in one place — see TBM Funded 2-Phase Challenge Rules.

Risk disclaimer: Trading forex and CFDs carries real risk and can result in loss of your capital. Prop firm challenges involve fees and don't guarantee funding or income. This isn't financial, legal, or tax advice — see our full Risk Disclosure.