How to Choose Between Prop Firm Account Sizes

How to Choose Between Prop Firm Account Sizes: A Practical Framework

How to choose between prop firm account sizes is a question most traders answer backwards — they pick the biggest number they can afford, not the size their actual trading supports. That's the wrong starting point.

The account size you evaluate for should match your current skill and risk tolerance, not your ambition. Go too big before you're ready and you'll blow the drawdown limit before you've proven anything. Go too small forever and you'll be leaving real profit on the table once you're consistent.

How to choose between prop firm account sizes: start with three questions

Before you look at a single pricing page, answer these honestly.

How much have you actually traded — real or demo? If you've got a live or demo track record showing consistent, controlled trades over weeks (not days), you can reasonably size up. If you're new to structured evaluations, start smaller. The rules are identical at every size — same drawdown percentages, same targets — so a bigger account doesn't make passing easier. It just raises the stakes on the same test.

What's your risk tolerance under a hard drawdown limit? A 10% max drawdown on a $5,000 evaluation and a 10% max drawdown on a $100,000 evaluation feel completely different psychologically, even though the percentage is identical. Bigger dollar swings on the same screen mess with people's heads. This is really a position sizing question wearing a different hat — know your own tolerance before you commit to a fee, not after a bad session.

Can you comfortably afford the entry fee if you fail once? Evaluations aren't guaranteed passes — nobody's are. Choose a size where a failed attempt doesn't put real financial pressure on you, because trading under financial pressure is exactly what causes drawdown breaches.

The fee-vs-size tradeoff nobody explains

Here's the part most guides skip: a bigger account size doesn't cost proportionally more. It costs less proportionally, because the fee is a fraction of a percent of the capital you'd be trading.

That sounds like "always go big" — it isn't. The fee is a small, fixed cost either way. The real cost of going too big too soon is the failed attempt itself, plus a second fee to try again. Sizing correctly the first time is cheaper than sizing ambitiously and resetting twice — good risk management applies to picking the account, not just trading it.

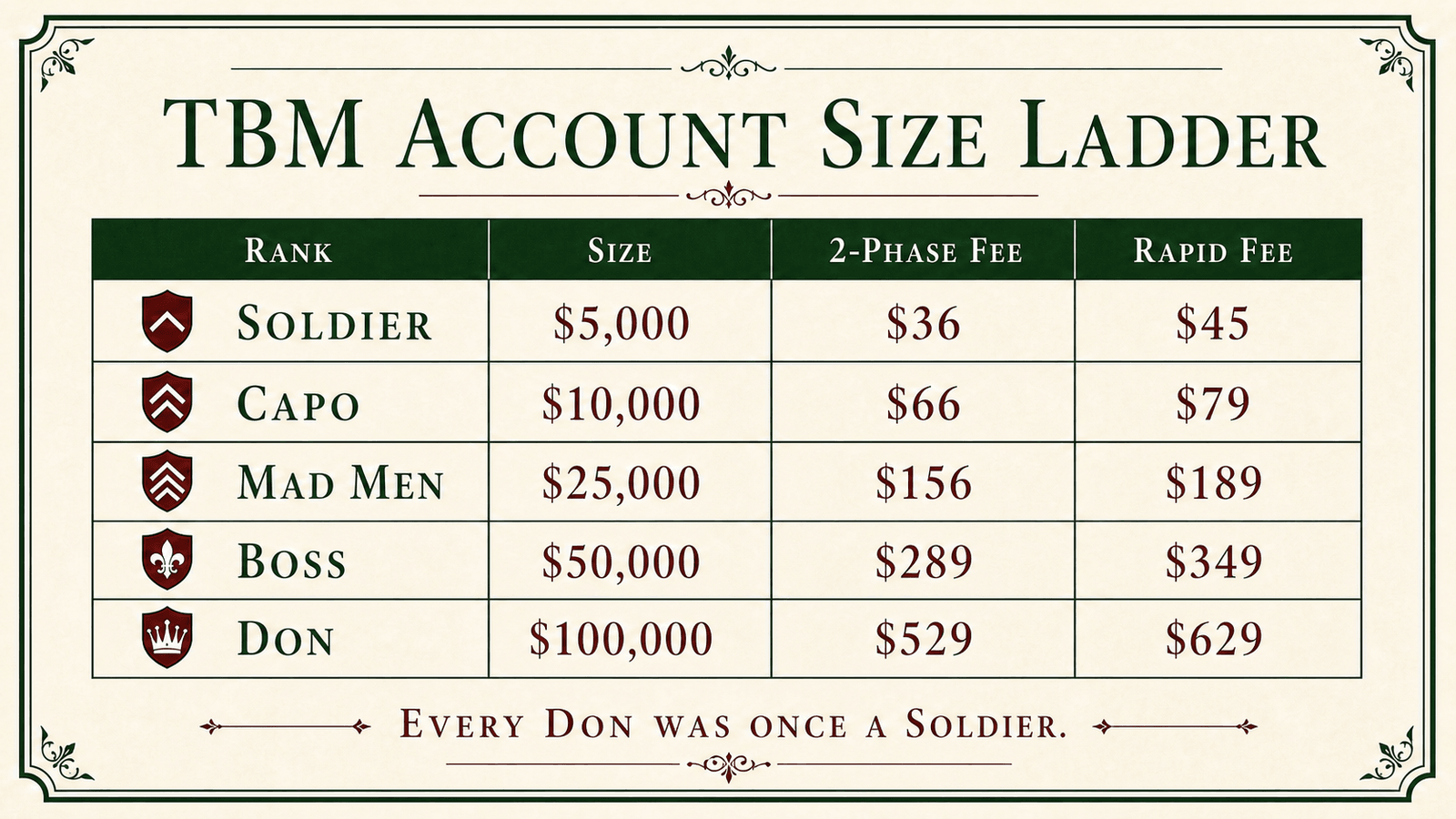

TBM's account size ladder, as a real example

TBM Funded runs the same rank ladder across two products — 2-Phase (the standard evaluation) and 2-Phase Rapid (tighter rules, faster pace). Both use identical percentage targets and drawdown limits at every size. Only the dollar amount and the fee change.

| Rank | Size | 2-Phase Fee | Rapid Fee |

|---|---|---|---|

| Soldier | $5,000 | $36 | $45 |

| Capo | $10,000 | $66 | $79 |

| Mad Men | $25,000 | $156 | $189 |

| Boss | $50,000 | $289 | $349 |

| Don | $100,000 | $529 | $629 |

"Every Don was once a Soldier" isn't just a tagline — it's the actual recommended path. Most traders new to prop evaluations start at Soldier ($5,000) or Capo ($10,000), prove they can hit an 8% then 5% target on 2-Phase (or 6%/6% on Rapid) without breaching a 10% (or 6%) drawdown, then reset up a tier once they've done it cleanly. A trader with a longer, verifiable track record of controlled risk can reasonably start at Mad Men ($25,000) or higher — the rules don't scale in difficulty, but your comfort with the dollar swings should.

The trading terms stay the same across every size too — same 1:100 leverage whether you're on Soldier or Don, only the fee and the dollar amounts change. Full targets, drawdown, and minimum trading day rules for both products are on Pricing and broken down in detail in our 2-Phase Challenge rules guide.

The two mistakes that actually cost people money

Over-sizing before proving consistency. Buying a Don-sized evaluation on your first attempt because the profit split math looks better is the single most common way people burn multiple entry fees. The percentage targets are the same at every size — a $100,000 account demands the exact same discipline as a $5,000 one, just with more zeros on the screen. If you haven't proven you can hold that discipline at a smaller size, a bigger account doesn't fix that. It just makes the mistake more expensive.

Under-sizing forever. The opposite mistake is real too. Traders who've clearly proven consistency at Soldier or Capo sometimes stay there out of caution, leaving profit on the table. The payout math tells the story: an 80% split on a $50,000 funded account pays out meaningfully more per winning cycle than the same percentage return on a $5,000 one. If your evaluation attempts are clean — hitting targets without drawdown warnings, respecting the consistency rule — that's the signal to size up, not a reason to stay small forever.

A simple way to decide

If you're unsure, work backwards from your comfort with the dollar amount, not the percentage. Think of it as a ladder you climb one proven step at a time, not a single all-or-nothing bet:

- New to structured evaluations, or new to trading discipline generally → Soldier or Capo

- Have a demo or live track record of a few consistent months, comfortable with moderate dollar swings → Mad Men

- Proven consistency across at least one prior pass, comfortable managing larger dollar drawdowns calmly → Boss or Don

None of this changes the rules you're evaluated against — the full rulebook is identical at every tier. It only changes what feels manageable while you follow it. And remember the account itself is always simulated capital — you never deposit your own money to trade it, you're only paying the one-time evaluation fee for the size you choose. That's the whole point of starting smaller: the downside of a miscalculated size is a fee, never your own trading capital sitting exposed in someone else's account.

Quick questions

Does a bigger account size mean a bigger profit split? No. On TBM, the split is set by product, not size — 80% on 2-Phase, up to 90% on Rapid, at every tier from Soldier to Don. Size changes the dollar amounts you're trading, not your split percentage.

Should I always start with the smallest account size? Not necessarily. Start small if you're new to evaluations or unsure of your discipline under real drawdown pressure. If you've already proven consistency elsewhere, starting at a mid tier like Mad Men is reasonable.

Is it cheaper to reset at the same size or pay to move up a tier? A reset (restarting a failed evaluation at the same size) and a fresh purchase at a bigger size are two separate transactions with separate fees. If you failed due to a rule slip rather than the size itself, reset first before jumping bigger — moving up doesn't fix a discipline problem.

Do the drawdown rules get easier at smaller account sizes? No. Every rule — profit targets, max drawdown, daily drawdown, minimum trading days — is identical across all five sizes on both products. Only the dollar amount and fee scale with size.

More common questions like these are answered in our full FAQ.

Risk disclaimer: Trading forex and CFDs carries real risk and can result in loss of your capital. Prop firm challenges involve fees and don't guarantee funding or income. This isn't financial, legal, or tax advice — see our full Risk Disclosure.